Share This Article

Cost center budget guidance does not seem all that complicated at first blush. It’s the percent increase or decrease a Town cost center gets for its operating budget from one fiscal year to the next. Sudbury boards typically talk about the three major cost centers: the Town of Sudbury, Lincoln-Sudbury Regional High School (LSRHS), and Sudbury Public Schools (SPS).

What’s somewhat unique in Sudbury is that it has a K-8 school district and it’s a member of a regional high school district. Regional school finance is similar, but in some ways very distinct from the more common Town-operated schools department like SPS.

Variances in the guidance between Sudbury’s three cost centers has generated controversy in recent years, with some elected and appointed officials questioning if SPS and LSRHS were being treated equitably with guidance and forecasted guidance from the Town Manager.

The problem, however, is that SPS expenses exist in both the SPS budget and the Town of Sudbury budget, whereas LSRHS is largely self-contained as a regional district. Put simply, SPS employee benefits and Other Post-Employment Benefits (OPEB) contributions are funded out of the Town of Sudbury budget. A simple percentage guidance, therefore, didn’t tell the whole story about Sudbury’s cost centers.

Apples to Apples

Mike Joachim, co-chair of the Sudbury Finance Committee (FinCom), has delivered several clarifying presentations on complicated municipal finance matters in recent years. On Tuesday, March 25, he was tasked with presenting the FinCom’s positions on Town Meeting articles, including the Fiscal Year 2026 budget, to the Select Board. Joachim shined new light on the ongoing discussions about cost center guidance on Tuesday.

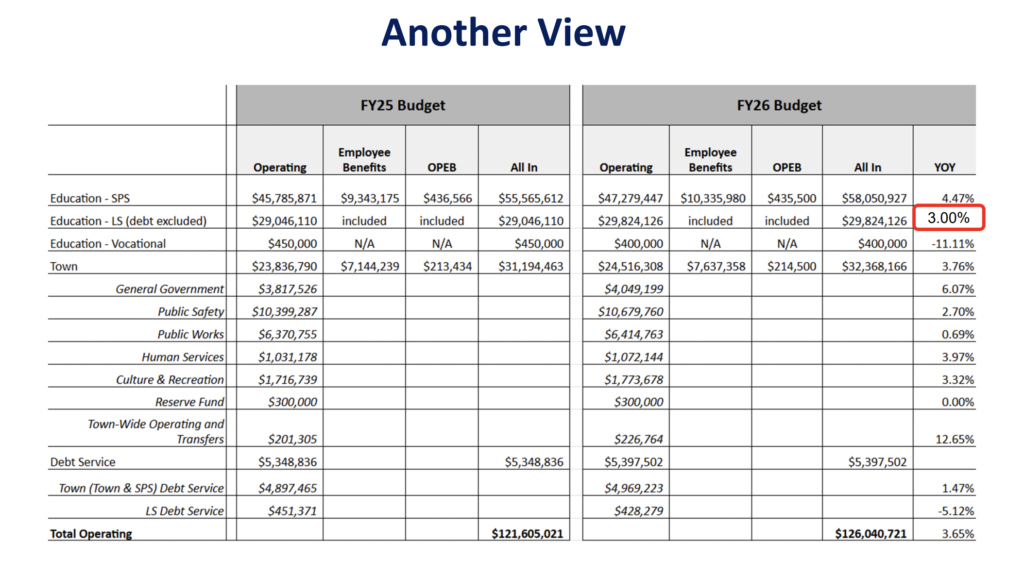

During his presentation, he offered a new way to look at guidance across the three cost centers. He separated capital budgets from operating budgets, added the SPS share of employee benefits and OPEB to the SPS budget, and removed the SPS share from the Town of Sudbury budget. Finally, he adjusted the LSRHS guidance to reflect that LSRHS didn’t need the full guidance provided by the Town in Fiscal Year 2025. The result demonstrated what he, and many members of the joint meeting, felt was a better “apples to apples” comparison of cost center guidance:

When calculated using Joachim’s method, SPS has the largest year-over-year guidance of the three cost centers at 4.47%. LSRHS had the lowest at 3.00%, and the Town of Sudbury was in between the two at 3.76%. Joachim’s full FinCom presentation is available here and embedded below.

Joachim has previously called out that varying guidance between cost centers isn’t necessarily a bad thing, but emphasized that clear communication is critical.

While the new presentation of the guidance helps, there’s considerable nuance in municipal finance. Town Manager Andy Sheehan has previously called for a “one community” approach to the budget, and highlighted the interconnected nature of Town services during is most recent Financial Condition of the Town presentation. “So I think it’s really important that people understand that as well. Because if you reduce services or budget on the town side, you’re reducing those services to the schools. You’ve got to get to school on safe roads, you’ve got to have safety, all those things. I think sometimes people forget that.” (2:40:00)